Cash is king

How I wish I had a mountain of cash to plow into this market. There are bargains everywhere I look. Here are some of them:

GOOG - $375. Google's last earnings release blew away market expectations but after a brief rally the market decided it was still bored of GOOG. I think GOOG can do $10 per share this year so that puts it on a 2006 PE of 37.5. That is a high multiple but when you think that GOOG's revenue growth is still in the high double figures it obviously deserves a premium rating. GOOG keeps gaining search market share in a growing market environment. When it start tweaking its other products to generate revenue the sky is the limit.

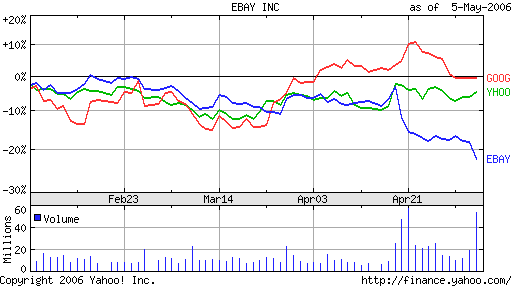

EBAY - $30. At the start of the year I never dreamt that eBay could dip this far. But it has, mainly as part of a general sell-off of internet stocks. So it is now on a 2006 PE of 30 and revenue is still growing at 35%. If you consider the protective moat eBay has around its business you have a screaming buy. I already have bought my full quota of eBay and more - unfortunately when it was over $40. But it really does seem to have bottomed out now. I have been calling eBay a buy all the way down from $46 and I still think that long term I am right. But at $30 eBay is a five star, A++++ buy.

Verisign - $21.50. For about five minutes in April I actually was in the black on my VRSN shares. Then the earnings release came out and the market decided that it was rather boring. So a month later VRSN is back hobbling around $21. Analysts struggle with VRSN because it has its fingers in too many pies. But just look at the figures: EPS of $1 in 2006. $3 a share in cash. Subtracting the cash gives it a 2006 PE of 18 - about the same as the growth rate. $1 billion share buy back just announced. That is almost one fifth of the market cap! VRSN is an investment of the highest quality. I already have some but at these prices I would like more.

There are three bargains without even trying. What about Intel? What about Microsoft? What about ARM holdings? What about CSR? What about Dana Petroleum? I really could have a shopping spree in this market!

posted by Phil @ 6:13 am

0 comments

![]()

![]()