Carnage

Ouch that hurt!

My growth portfolio down 6% in one day! CSR got the day off to a bad start with a great (!) earning report which obviously did not live up to market expectations and the stock finished down 13%, wiping off all my gains on this one. And to think I was up 30% a month ago!

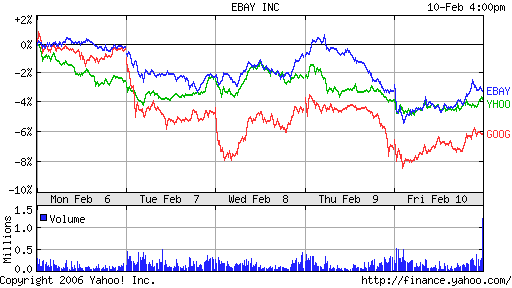

Then the Google CFO happened to mention something about slowing growth and it got caned, along with most of the other Internet stocks.

The only good news was in my mortgage portfolio where RBS issued a great report (increased dividends, buybacks starting) and shot up almost 3%.

BTW I must comment on a pathetic Forbes article about Google's valuation. The article is here. I can't believe that the author used Yahoo's current trailing PE of 22 to compare against Google's. How any so called internet stock analyst look at Yahoo's trailing PE and not have the words "skewed by one-time items, not useful for comparisons" scream at them is beyond me. The forward PE is over 40 for goodness sake. The whole article is just repeating what journalists have been saying for months anyway. Can't they find something new to write about? It is not that I mind hearing the bear case for Google but to talk about its PE and price-to-sales ratios without talking about its growth rate is just meaningless.

Anyway rant over.

Tomorrow has to be a better day for my stocks... doesn't it?

posted by Phil @ 10:59 pm

0 comments

![]()

![]()