What a load of rubbish

The way technology stocks have sunk in the last six months is quite spectacular. Here is a chart for a few of the bellwethers:

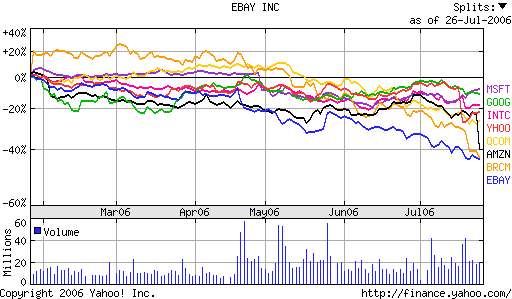

Ebay's decline has been so spectacular it deserves its own chart:

Talk about a shorter's dream. At least eBay is consistent I suppose. I never dreamed eBay could go below $25 but I guess I am learning more about the stockmarket every day. One thing that stood out from their recent earnings conference call was that organic revenue growth was only 21% year on year. That is much less than the market is used to and partly explains why the trailing PE is down to 30 from well over 100 2 years ago.

For some of the eight stocks in the first chart this is a tremendous buying opportunity. But which ones? Google and Qualcomm would be my best guesses but in the current market even these could fall another 10% for no good reason.

Nevertheless after 6 months of pain us tech investors must be due a little bit of joy?

posted by Phil @ 5:44 am

0 comments

![]()

![]()